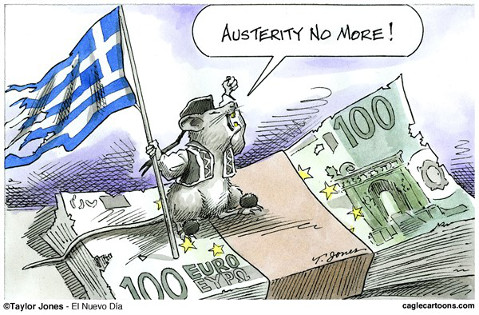

The Rejection of Austerity in Greece

Voters Rally Behind Alexis Tsipras, Newly Elected Prime Minister

New prime minister of Greece Alexis Tsipras takes office amid a complex financial crisis, winning on a platform that rejected the austerity imposed by European central bankers. Greece — like Spain and Portugal — had spent the late 20th century catching up to the rest of Europe in economic and political terms, creating (relatively) modern, prosperous economies and (often rather fragile) democratic governments.

Abandoning the drachma for the euro in 2001 was supposed to mark Greece’s graduation to mature European nationhood. And for a time things went quite well, with low European interest rates (anchored by the Germans) sending billions into Mediterranean businesses, real estate, and sovereign bonds.

The Greek economy was (and is) a small, opaque, and comparatively fragile system, but the tsunami that struck in 2008 came not from Greece’s weaknesses but the U.S.’s ostensible strengths as the world’s deepest, richest, and supposedly smartest capital markets — and what turned out to be Wall Street’s enormous overreach.

Greece had, to be sure, borrowed heavily since the 1990s — but it also had Europe’s best GDP growth rate (over 4 percent) to show for it. Absent Wall Street’s meltdown, Athens probably could have navigated a less-severe recession. But when the entire Western financial system started to topple in 2008, Greece — a minor, minor player — was doomed to became roadkill. Tourism and shipping — the country’s two biggest earners — dried up while oil prices (Greece imports all its oil) soared. As the economy contracted sharply, new investment dried up, bankers stopped lending, and government revenues plummeted. In late 2009, the newly elected Papandreou government learned that it was inheriting a budget deficit of 15 percent of GDP.

Papandreou entered office just two years after Lehman’s collapse — and by then Europe’s biggest banks were in a zombie-like trance, with their commercial and real estate loan portfolios worth in some cases half their book value. Until then regulators had let banks count government bonds as “riskless” and, hence, able to anchor the bankers’ risky portfolios and capitalization. But Greece’s budget crisis, and with it the desperate need to borrow to plug the deficit, made people realize overnight that European sovereign debt was anything but riskless — and that the banks would topple if forced to admit their effective systemic bankruptcy.

For Europe, saving Greece in May 2010, when it began pouring billions of euros into the country, wasn’t about saving Greece — it was about saving the continent’s most powerful, politically connected banks, and ultimately the European economy. (Greece by itself is just 2 percent of Europe’s GDP; its debt 3 percent. The fear was that Spain or even Italy might contract “the Greek disease.”) Most of the money Europe and the IMF (International Monetary Fund) sent to Athens consequently did nothing to spark Greece’s economic recovery; instead the cash U-turned almost immediately and flowed right back to the big banks holding Greek bonds.

But fearful politicians and an alarmist press framed “the rescue” to beleaguered voters as an Aesopian tale of the industrious (northern) ant rescuing the shiftless (southern) grasshopper. It was a fable — but, as Aesop knew, fables of all sorts are an essential ingredient in our lives, and this one stuck. Millions of Greeks struck back with fables of their own — about “fascist finance” that recalled the painful Nazi occupation of Greece in World War II, portraying Greece as the hapless and innocent victim of foreign invaders in league with Greek oligarchs.

The Troika

What came with the loans — and stayed in Greece, unlike the loans themselves — was “the Troika” — technocrats sent by the IMF, European Central Bank (ECB), and Brussels. They were armed with detailed and comprehensive lists of what Greeks — the government, employers and employees, retirees, education, health care, agriculture, etc. — all were expected to reform in exchange for Europe’s financial aid.

Greece’s government and economy desperately needed reform — Papandreou had been elected on a promise to do just that. But reforms carried out by a popularly elected government aren’t the same as those imposed by unelected and uninvited foreigners, in Greece or anywhere else.

From the start, the reforms rested on projections of quick recovery that proved wildly wrong. Forced to take the bitter medicine, the Greek economy grew sicker and sicker — and remains so today, six years after the start of the Great Recession, the sickest economy in Western Europe, with only the weakest prospects of recovery even now still in sight.

In fairly short order, Greece burned through three governments — the left-of-center Papandreou regime, a caretaker period overseen by a former central banker, and for the last two years, the right-of-center Samaras government, which fell last week to the anger most Greeks now feel toward the established political order across the spectrum.

‘The Era of National Humiliation Is Over’

A friend in Athens — a veteran former cabinet minister and economist who’s quite sympathetic to Tsipras’s goals — called me the night of the Greek elections. “Tonight,” he said dryly, “is going to be the happiest moment of the rest of Tsipras’s life.” Tsipras, on the other hand, optimistically proclaimed that “the era of national humiliation is over.”

Tsipras and his top ministers believe what they’ve believed since 2010 — that Europe can be “faced down” over debt relief — and that all the suffering the Greeks have lived through resulted from the cowardice of their political predecessors.

But that may not necessarily be the case. Most of Greece’s debt is now held by public institutions, not banks, so the concern in 2010 over Greece possibly defaulting on its loans no longer threatens the financial system. The governments and IMF as a practical matter could certain absorb, say, a 50 percent write-down of Greek debt without real technical difficulty. The real problem of such a write-down goes back to Aesop and fables again: It’s not clear that voters, who’ve been told they’re the hardworking ants, won’t punish political leaders whom they see as indulgent, shiftless grasshoppers. In that fundamental sense the New Greek Debt Crisis is a political crisis, not the economic one it was four years ago.

I’m certainly hopeful Tsipras and the Troika can strike a deal both can live with. The question is whether that deal will restore real growth, and with it rapidly declining unemployment and a new national confidence in the future.

Greece certainly needs debt relief. The austerians have been and still are just dead wrong about their prescriptive advice. The U.S. is recovering now much faster than Europe because we ignored that sort of advice — and frankly we’d be even further along in recovering if we’d ignored it sooner and more vigorously — but that’s another story. We have our own fables to deal with.

But Greece needs more. It needs a banking system that will start to lend — at a time when a third or more of outstanding loans in Greek banks are nonperforming. Tourism and shipping need to recover — and both are determined by wider, global markets, not what the Greeks do. The reform of Greek government and business practices is a work in progress — far more has been done than outsiders give Athens credit for — but there’s still an enormous amount to be done.

Key to that reform is better tax collection, especially from the well-to-do — and it’s not yet clear that’s going to be quick or easy. The Papandreou government I advised was just as committed to tax reform and collection — and I saw from the inside the myriad problems, from poorly trained tax officials to a glacially slow court system, that made an efficient, modern tax system mercurially elusive, despite real efforts and the best intentions. Organized capital can go on strike just as organized labor can — and we’re about to see whether that’s going to happen in Athens.

Even if Tsipras negotiates a fairly hopeful package of debt reduction, all those other issues will still face him. Neither he nor several of his key ministers has actually run a government before, let alone reformed one amidst a crisis like this.

Greece is likely to live through a rolling series of crises ahead, shaped by its internal and external weaknesses and vulnerabilities. No one should expect Greece to look hale, prosperous, and happy any time soon.

The Gini Coefficient

Politically, Europe and the U.S. are entering a new era. For the past 60 years, we’ve all focused on one number — the GDP growth rate — to measure our economic success. Going forward, we need a second — the Gini coefficient — to measure who’s benefitting from all that growth beyond the top one percent. President Kennedy’s famous promise, “rising tide lifts all boats,” hasn’t been true for the past 40 years — and millions of voters are now waking up to that reality. That’s going to generate some truly wrenching transitions on many fronts, and they’re only now just beginning.

In the past 30 days, we’ve seen the horrific murders in Paris and a rising backlash against immigrants, Mario Draghi’s announcement of what’s supposed to be the ECB’s version of quantitative easing, the continued fall of oil prices that are heightening tensions with Putin’s Russia, and here in the U.S., the Republicans’ new control of Congress alongside a lame-duck president.

Tsipras’s election in Athens — a game-changer in Greece in several ways — is thus just the latest shock to the European system. How Berlin and Brussels (and Paris and London) cope with all this just can’t be predicted safely in advance. There are just too many moving parts in the Rube Goldberg contraption called the European Community.

European Stability

Like the U.S., Europe now navigates a new world order in which the two North Atlantic superpowers of the last several centuries are no longer calling the shots for everyone else. Greece is one more (albeit in extremis) reminder that we’re nowhere near The End of History.

It may be more like The Beginnings of a New History, with a new Quadrilateral of Issues shaping global politics going forward, a politics in which no individual nation operates freely. Inequality, corruption, big data, and the environment are going to provide the core frame for that politics — and how the U.S., Europe, China, Russia, India, Brazil, and the rest of the New Great Power system address them is the ongoing and open question of our young century.

Richard Parker, an Oxford-trained economist teaching at Harvard’s Kennedy School of Government, advised the Papandreou government on economic reforms from 2009-2011, is the biographer of John Kenneth Galbraith, the former president of Americans for Democratic Action, and is a cofounder of Mother Jones magazine and The Santa Barbara Independent.