“I believe that the greatest gift you can give your family and the world is a healthy you.” —Joyce Meyer, Charismatic Christian author and speaker

If you ever sat in an emergency room waiting to hear news about a loved one in the middle of the night or stayed in a hospital bed for weeks at a time, away from your family and apprehensive about your livelihood, you know the feeling of hopelessness. In modern America, should there still be uncertainty about being able to regain one’s health? In America today, for many, these misgivings have not been eased.

If you have ever had to choose preventive care or treatment to cure or manage an illness and as a consequence go without the essentials of life — food, clothing, paying utility bills or mortgage — you understand the black hole of having inadequate health insurance coverage. The U.S. health-care system and the financial strain it places on poor and middle-class families is morally bankrupt for a nation that purports American exceptional ism.

The Affordable Care Act that was passed in 2010 by both houses of Congress and signed into law by the President of the United States has become a monumental wedge issue between the right and the left in this country. Led by an obstructionist Tea Party Republicans, a faction in Congress has tried and failed to appeal the law over 60 times (with the 61st time already in the works). The first 50 failed attempts cost the taxpayer $75 million.

The Obama administration has added fuel to this brimstone obstructionism with promises like “If you like your plan (health insurance) you can keep your plan.” And the website rollout just revived “Reaganesque” rhetoric of big government dysfunction compared to “free” market capitalism.

In recent polling, the second leading candidate for the Republican presidential nomination, Ben Carson, has characterized the law as the “worst thing that has happened to the nation since slavery.”

So where does the truth lie? Where are we today in the goal to bring health-care costs down by encouraging preventive care in all the people who are newly insured?

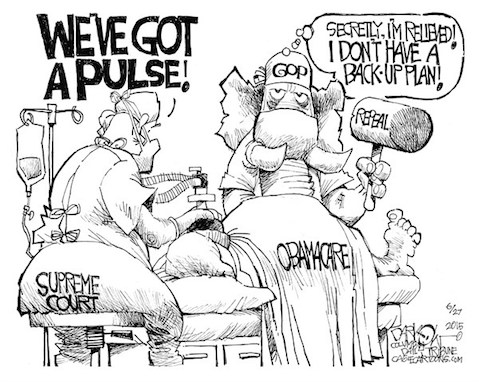

In March 2015, Health and Human Services reported a total of 16.4 million people covered between the Affordable Care Act marketplace and Medicaid expansion. In a nongovernment report, RAND (Research and Development) Corporation estimated that 22.8 million people have received coverage since the inception of the law, while 5.9 million people lost their health plan, which equals a net gain of 16.9 million people insured for health care. The uninsured rate, according to the Centers for Disease Control, has gone down from 15.7 percent to 9.2 percent since 2013. For the proponents of the law, the figures highlight the initial success and viability of the program. For many on the right side of the aisle in Congress, this not enough. A common catch phrase for Republicans remains “repeal and replace Obamacare.”

A June 2015 article by Ramesh Ponnuru in the National Review (a semi-monthly magazine founded by conservative pioneer William F. Buckley) on the question of nationwide coverage said, “Conservatives are ambivalent, at best … They should nevertheless overcome their ambivalence. There are good reasons to embrace a conservative health-care policy … not the least being that in the present political context, that policy might be the best way to restrain both costs and government.”

Now, some GOP candidates on the campaign trail are echoing two alternatives to the Affordable Care Act that speak to the irresoluteness that Ponnuru mentions in his article.

Presidential hopeful Marco Rubio and Congressmember Paul Ryan have presented alternative plans similar to what Republicans have preached since 2010. The two common denominators are insurance companies being able to sell health-insurance policies over state lines (a national market rather than individual state markets) and tax credits for the consumers to buy insurance. While their ideas, if implemented, may provide relief from higher premiums, their expectations of these plans being propagated are unrealistic.

In a New York Times article, the lobbying group America’s Health Insurance Plans and the Blue Cross and Blue Shield Association expressed little enthusiasm among the big five health-insurance companies in setting up across-state-line plans. Initial and long-term costs of creating and maintaining offices in different states and complying with different state regulations have discouraged the notion that multi-state insurance would be a better profit model then what’s currently in place. And while tax credits to individuals to buy health insurance seem credible on the surface, the Republican plan gives no mention of how it would provide insurance for those who are below or even moderately above the poverty line and don’t pay federal income taxes to begin with.

Though some insurance premiums have risen under the new law, without a government single-payer system in place, insurance companies have and will continue to raise premiums. This despite soaring profits from all the new customers, according to a 2015 CNN report, for all the big five health insurers — Aetna, Anthem Blue Shield, Cigna, Humana, and United Health. Their rise in stock price has beaten expectations and the S&P 500 over the last five years. In addition, from 2000-2008, health-insurance rates continued to rise at a record pace well before the Affordable Care Act came into existence. Marinan R. Williams, chief executive of the Scott & White Health Plan in Texas, commented recently regarding the company’s ask for a 32 percent premium increase next year, “The requests for services showed there was a real need for the Affordable Care Act. There was a pent-up demand, and over the next three years, I hope rates will start to stabilize.”

Today, affordable and quality health care for all is still stuck at the crossroads of political partisanship. Recently Republicans were given a reprieve in their efforts to dismantle the Affordable Care Act: a lawsuit against President Obama claiming his administration spent money for health insurers (for waiving co-payments and other costs for new policyholders) without receiving congressional countenance. As lead counsel Jonathan Hurley for the Republican-led House expressed, the case hinges on “the power of the purse.” While many legal experts see this kind of lawsuit as unprecedented in settling partisan political fights between two branches of the federal government, congressional Republicans remain undaunted in their attempts to repeal “Obamacare,” their holy grail of opposition for a party that interprets the law’s success as a recipe for electoral disaster for years to come.

And in the flurry of vitriol that casts the law as socialist — when private insurance companies are still very much in control — and the incessant hyperbole of inescapably ignorant buzz phrases like “death panel” and “sticker shock” that pervade the air waves, one word fails to be inserted into the dialogue by the GOP: compassion.

When the United States, with the vast resources we possess, cannot coalesce around viable solutions to provide quality health care for its people, we show an unenviable weakness to the rest of the world. Surely the lives of those already born in this country are worth more than the cost to provide treatment. Surely citizens should not agonize in their decision to be whole physically and mentally and also face economic instability. The Affordable Care Act brought meaningful change for people with pre-existing conditions and protected them from rendering their insurance ineffective due to lifetime caps. The law was built and passed quickly, improvements are warranted, but for the first time in our history we have a foundation to build on.